Look, you already know chargebacks are a problem.

You're not here for a lecture about why they matter—you're here because you want to know if your rate is normal or if you're actually screwed.

So what's the average chargeback rate for eCommerce? What are other stores dealing with? And at what point does your payment processor start making your life hell?

Let's cut through the noise and get to the actual numbers.

What Is a Chargeback?

A chargeback is when a customer disputes a charge with their bank or credit card company, and the bank reverses the payment—pulling the money back out of your account.

It's not a refund.

With a refund, the customer comes to you, you agree to give their money back, and you part ways.

With a chargeback, they skip you entirely and go straight to their bank.

The bank sides with them by default, and you're left scrambling to prove the transaction was legitimate.

Here's the kicker: even if you win the dispute (which is rare), you still eat the chargeback fee. And the chargeback still counts against your rate.

The process goes like this:

Customer files dispute → Bank issues chargeback → Money gets yanked from your account → You get a notification and a fee → You have a short window to fight it → You probably lose anyway.

It's designed to protect consumers, which sounds great until you're the one getting hit with fraudulent claims you can't do anything about.

What's the Average Ecommerce Chargeback Rate?

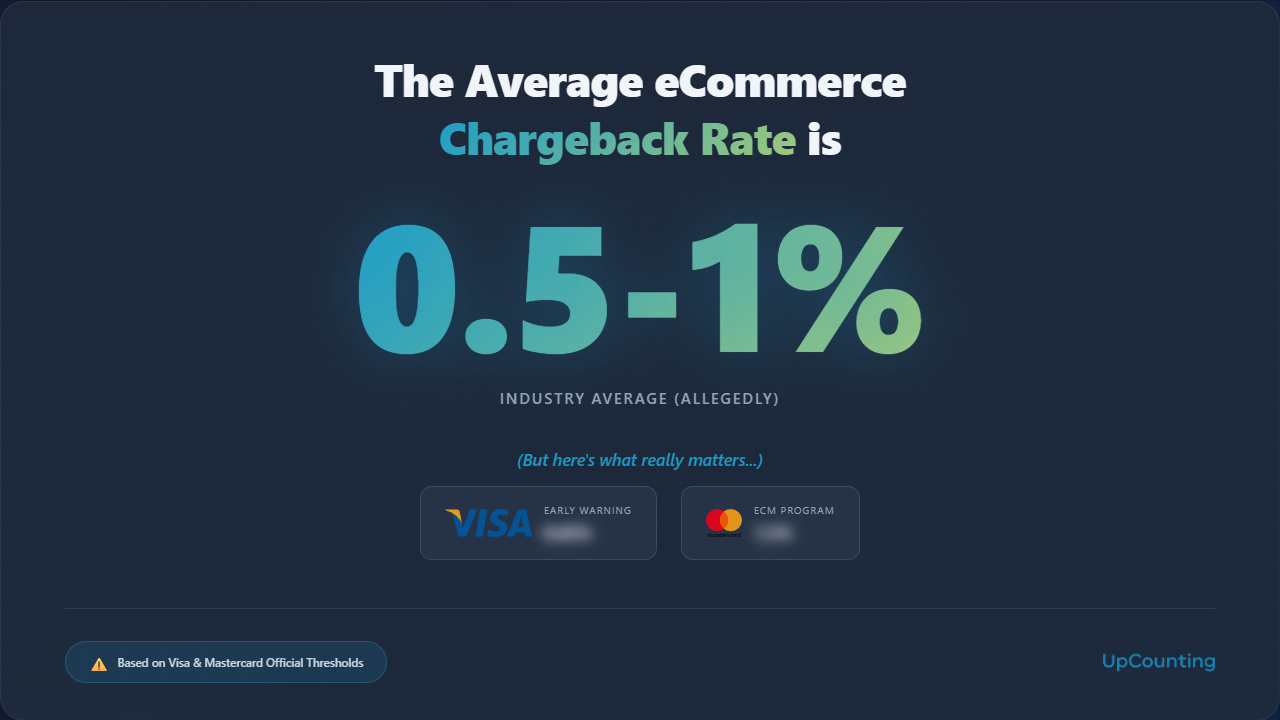

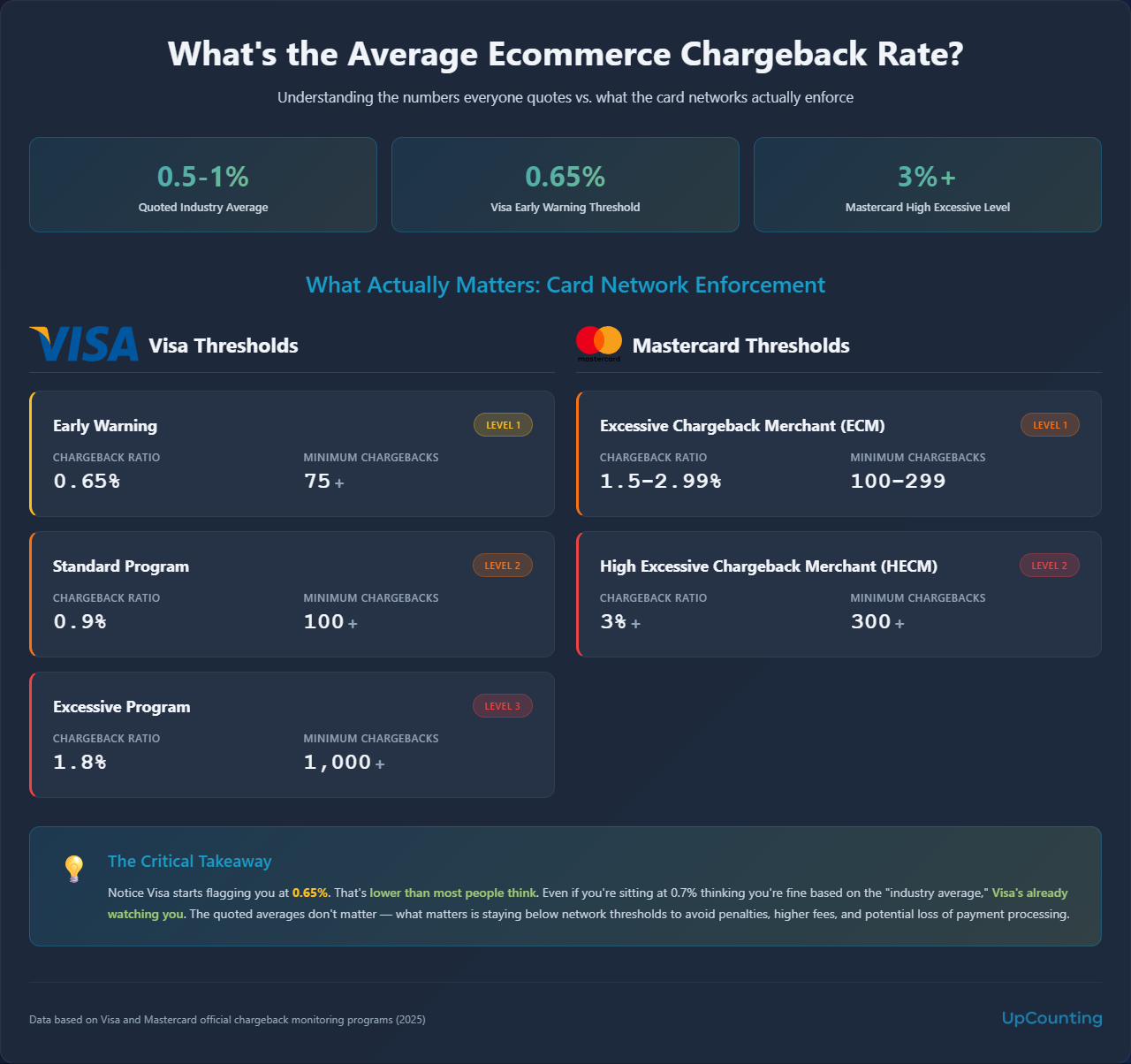

The average ecommerce chargeback rate is supposed to be around 0.5% to 1% (on paper).

However, there's no official source that actually tracks this across all merchants.

You'll see these numbers thrown around everywhere—from payment processors, consultants, industry surveys—but they're based on limited sample sizes and self-reported data.

What we do know for certain is what the card networks actually enforce. And that's what really matters.

Visa's thresholds:

- Early Warning: 0.65% ratio + 75 chargebacks per month

- Standard: 0.9% ratio + 100 chargebacks per month

- Excessive: 1.8% ratio + 1,000 chargebacks per month

Mastercard's thresholds:

- Excessive Chargeback Merchant: 1.5% to 2.99% ratio + 100-299 chargebacks per month

- High Excessive Chargeback Merchant: 3%+ ratio + 300+ chargebacks per month

Notice Visa starts flagging you at 0.65%. That's lower than most people think. Even if you're sitting at 0.7% thinking you're fine, Visa's already watching you.

So forget about comparing yourself to some mythical industry average.

These are the actual numbers that determine whether you're about to get hit with fines, increased fees, or lose your ability to process payments altogether.

If you're anywhere near these thresholds, you've got a problem—regardless of what everyone else is doing.

What’s the Average Chargeback Rate by The Ecommerce Industry?

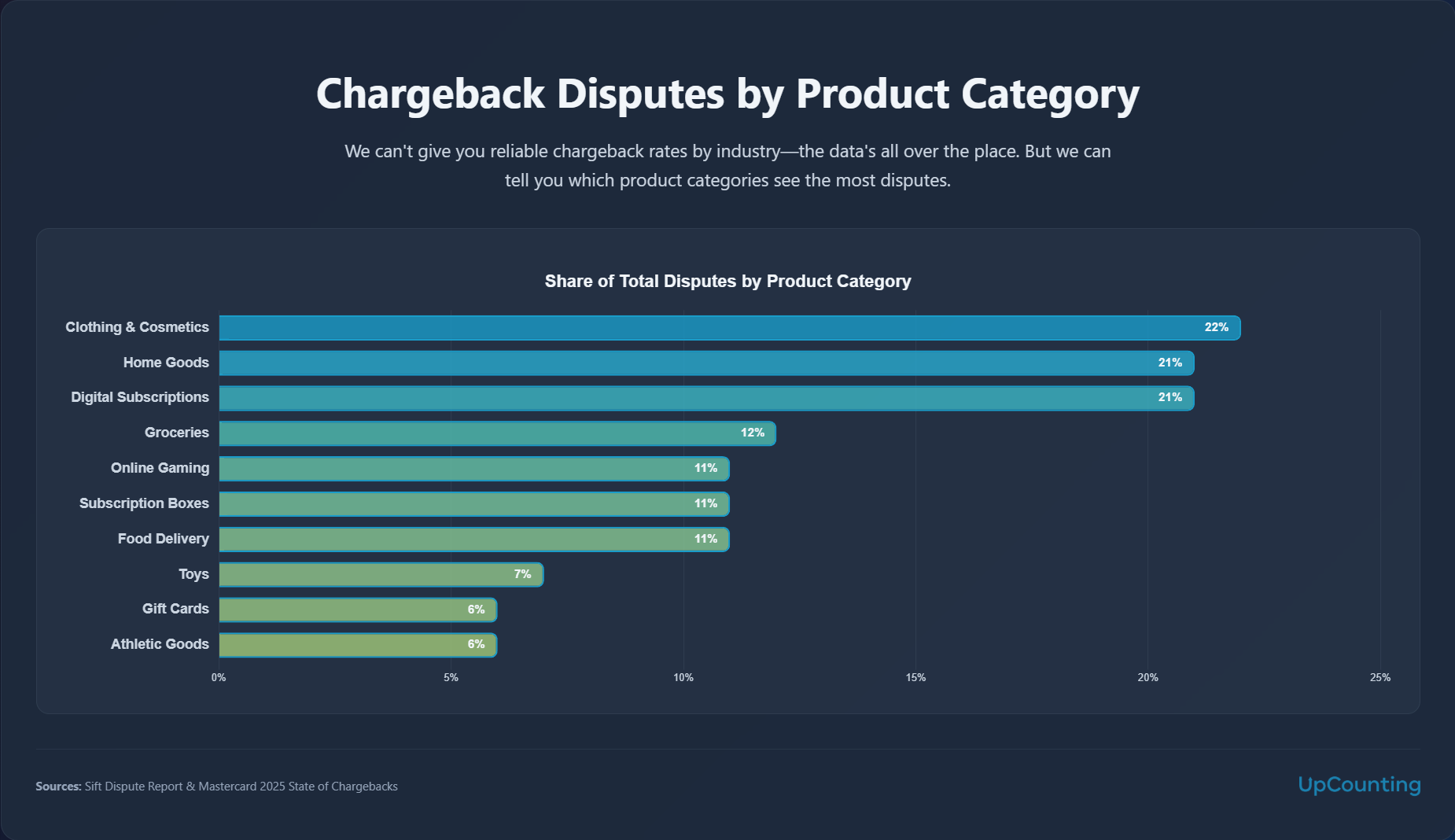

We can't give you reliable chargeback rates by industry—the data's all over the place with no solid sourcing.

But we can tell you which product categories see the most disputes, and that tells you a lot about where the pressure is.

According to dispute data from Sift, here's what gets disputed most often:

- Clothing, accessories, and cosmetics: 22% of disputes

- Home goods: 21% of disputes

- Subscriptions for digital apps and services: 21% of disputes

- Groceries: 12% of disputes

- Online gaming: 11% of disputes

- Subscriptions for physical goods: 11% of disputes

- Food deliveries and restaurants: 11% of disputes

- Toys: 7% of disputes

- Gift cards: 6% of disputes

- Athletic goods and equipment: 6% of disputes

Now, dispute volume is one thing, but dispute value is another.

According to Mastercard’s 2025 state of chargebacks report, Travel and hospitality sees the highest average chargeback value at $120 per dispute.

Part of the problem? Customers often book through third-party sites or travel agencies instead of directly with the hotel or airline.

So when something goes wrong—weather delays, sickness, cancelled plans—they don't reach out to the actual service provider. They just go straight to their bank and dispute the charge.

If you're in travel, you're not just dealing with more complex transactions—you're dealing with customers who don't even see you as the point of contact when issues arise.

The State of Chargebacks in 2025

Visa's latest research on eCommerce payments and fraud gives us a clearer picture of what's actually happening with chargebacks right now. And it's a mixed bag.

The good news: Fraud rates are actually down across the board.

After years of climbing, we're finally seeing declines in some of the most common attack types—card testing dropped, triangulation schemes dropped, and even first-party misuse (customers claiming they didn't make purchases they actually did) saw a significant decline.

This is notable because first-party misuse has been rising rapidly over the past two years. Seeing it drop suggests that merchants are finally getting better at fighting back.

The bad news: Nearly every merchant (98%) still dealt with at least one type of fraud in the past year.

So while individual fraud rates are down, the variety of attacks merchants face hasn't changed. You're still dealing with multiple threats at once.

The top five fraud threats hitting merchants right now are:

- Real-time payment fraud

- Refund and policy abuse

- Phishing attacks

- First-party misuse

- Card testing

Each of these impacts between one-third and half of all merchants globally. If you're running an eCommerce business, you've probably dealt with at least two or three of these in the past year.

What's changing on the merchant side

Merchants are getting smarter about fighting chargebacks.

Almost 90% now use "compelling evidence" to dispute fraudulent chargebacks—that's up from 83% last year.

More merchants are staying current on the latest dispute rules and submitting the full range of data points that can help win disputes: delivery confirmations, IP addresses, device fingerprints, customer communication records, all of it.

And it's working.

Merchants who use compelling evidence are seeing better dispute win rates and lower false rejection rates.

The ones who stay on top of it are starting to turn the tide.

The emerging problem

While first-party misuse might be declining, refund and policy abuse is rising fast.

Over half of merchants (57%) report increases, with more than one in five (22%) seeing spikes of 50% or more in just the past year.

What's driving it?

Customers are filing false claims that items never arrived, attempting to return used or damaged products, or exploiting lenient return policies.

This type of fraud doesn't always trigger a chargeback—it often bypasses that entirely—but it still eats into your margins and creates operational headaches.

According to Visa's data, merchants blame two things: customers learning how to "game the system," and issuing banks making it too easy to submit and win disputes.

That's a shift from previous years, when merchants pointed to inflation and changes in cardholder protections as the main drivers.

How merchants are responding

More are relying on technology to fight fraud instead of manual reviews.

The share of merchants manually screening orders is dropping, while digital fraud monitoring is increasing—especially at the refund and dispute stages, which jumped from 45% to 57% in just one year.

On top of that, over half of merchants are now using generative AI fraud tools, with many more planning to adopt them soon.

The focus for 2025? Improving the accuracy of AI and machine learning tools, and increasing automation in fraud prevention.

But it's not all smooth sailing.

Over 80% of merchants say they struggle with data and tech challenges—things like effectively using the data they have, improving AI accuracy, and dealing with gaps in their fraud tool capabilities.

Staying current on the latest threats and constantly adapting tools is an ongoing battle.

The spending trend

Looking ahead, 63% of merchants plan to increase spending on fraud and chargeback tools and technologies this year. Only about half plan to spend more on staff and talent.

The message is clear: merchants are betting on technology to solve this problem, not just throwing more people at it.

Chargebacks and fraud rates might be stabilizing or even declining in some areas, but fraud itself isn't going away—it's just shifting forms.

You're not fighting less fraud. You're fighting different fraud.

And if you're not adapting your tools and tactics to keep up, you're going to fall behind those thresholds we talked about earlier.

So Where Does That Leave You?

If you're sitting comfortably under 0.65%, keep doing what you're doing—but don't get complacent.

Fraud is shifting, and what works today might not work six months from now.

If you're hovering between 0.65% and 0.9%, you're in Visa's early warning zone. You're not in immediate danger, but you need to tighten things up now before you cross into territory that comes with actual penalties.

If you're above 1%, you need to treat this like the urgent problem it is. You're not just losing money on individual chargebacks—you're risking your entire payment processing setup.

The reality is this: there's no "safe" average to compare yourself to. The only numbers that matter are the card network thresholds, and they're lower than most people think. Focus on staying under those, invest in the right fraud prevention tools, and actually use compelling evidence when you dispute chargebacks.

Most importantly, stop waiting until you get a warning letter from your processor. By then, you're already behind. Check your chargeback rate now, understand where you stand, and fix it before it becomes a crisis.

Because once you're flagged, digging yourself out is a lot harder than preventing the problem in the first place.

.jpg)